PwC’s Global Entertainment & Media Outlook 2018-2022 says the evolution of the entertainment and media industries has entered a dynamic new phase:Convergence 3.0.

Five drivers identified behind the latest convergence with trust-building singled out as ‘vital’ by PwC’s latest Global Entertainment & Media Outlook. “Standing still is not an option” – rapid changes in the entertainment industry herald a dynamic new phase, says PwC.The competitive playing field is being redefined by what PwC is calling “Convergence 3.0”. They say it is different from previous waves of convergence in that it is seeing the rise of two groups. Firstly there’s the ever-expanding group of “supercompetitors”. This runs alongside specialized, niche brands which strive to entice ever more demanding consumers.

Borders between the technology and telecom industries and entertainment and media are dissolving. We’re seeing vertical integration between large Internet access providers and delivery platforms. Meanwhile the online giants are spreading their boundaries horizontally into content.

Lines between traditional segments are also becoming blurred as the likes of print and digital, social and traditional media, wireless and fixed access come together.

Broad-based yet uneven distribution of growth

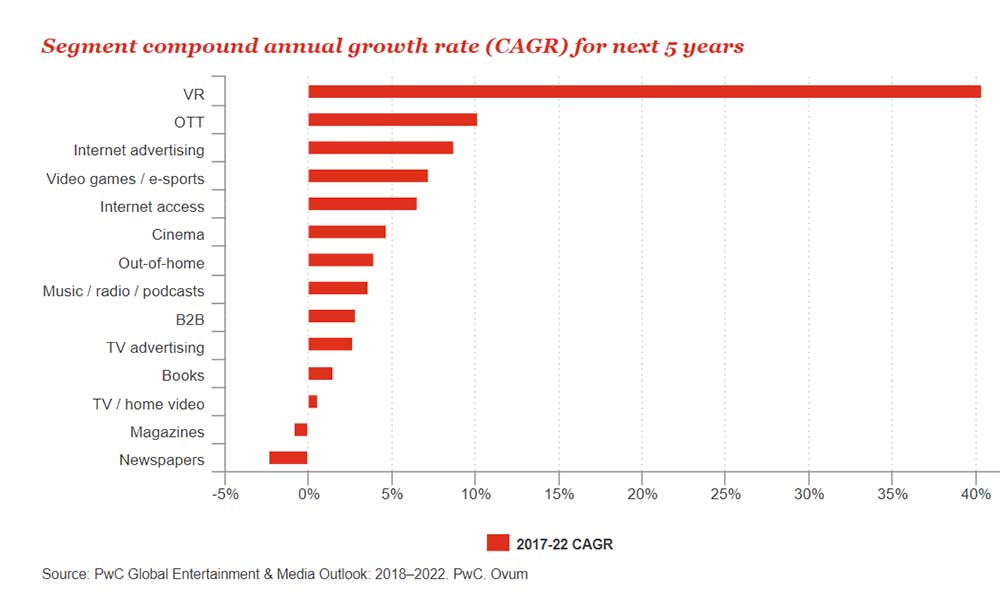

The Outlook projects overall global spending on entertainment and media will rise at a compound annual growth rate of 4.4 percent over the next five years. Global revenue will reach US$2.4 trillion in 2022 (a rise from US$1.9 trillion in 2017).However growth is unevenly distributed between various segments of the industry. Virtual reality leads the way with a five-year CAGR of 40.4 percent. After this comes OTT video with a CAGR of 10.1 percent. In stark contrast, traditional print media will see revenue dive over the next five years.

There are significant differences between sub-segments. While the overall CAGR for the video games and e-sports segment is 7.2 percent, e-sports specifically will jump by 20.6 percent compounded annually.

There are also regional differences across the world. While box office rose 4.3 percent across the globe in 2017, it fell in the US, France, and Australia. And while newspaper revenue is generally in decline, India will see an increase of around US$1 billion by 2022.

The fastest-rising entertainment markets through 2022 for overall spending will be Nigeria and Egypt, driven mainly by surging spending on Internet access. However, if you take out Internet access, India takes the lead with a 10.4 percent CAGR, followed by Indonesia at 8.4 percent.

“The story behind the Outlook’s global figures is a near-infinite accumulation of micro-stories, and a dizzying array of different trends, at a territory and segment level,” says Ennèl van Eeden, Global Entertainment & Media Leader, PwC Netherlands. “The pace of change isn’t going to let up: technologies such as artificial intelligence (AI) and augmented reality will continue to redefine the battleground.” He points out that technology enables content delivery to become progressively cheaper and more personalised. This, in turn, “heightens the urgency for companies to invest in technologies that will enable them to compete more effectively.”

Five key drivers

The Outlook has pinpointed five key drivers behind the latest convergence:- Ubiquitous connectivity: high-speed mobile Internet connections will increase by 2.2 billion globally by 2022. The tipping point will take place in 2020 - overall global data consumption via smartphones will leapfrog over fixed-broadband data consumption.

- Mobile consumers: mobile devices are becoming the primary way to access content and services across nearly all markets. 2018 will be the first year during which global mobile Internet advertising revenue will overtake its wired equivalent.

- The need for new sources of revenue growth: companies look beyond traditional revenue sources. Meanwhile telecom companies target entertainment and media content for growth revitalisation. OTT spending will grow at a CAGR of 10 percent through 2022 (as opposed to 2.3 percent for broadcast TV advertising).

- Value shift to platforms: social media and technology platforms outpace traditional content creators. Hence the rise of supercompetitors. Some traditional content companies are developing their own platform-like businesses.

- Personalisation: companies will use data analytics and AI to appeal to consumers who want a personalised experience. Live experiences will retain popularity. Ticket sales for e-sports events are set to rise at a CAGR of 21.1 percent through 2022.

Trust is vital

The Outlook stresses that building and earning consumer trust is absolutely vital. Trust in many industries is extremely low right now, so a company’s ability to maintain trust is a vital differentiator. Entertainment and media companies need to look at their trustworthiness across content and data, monetisation, social impact and how appropriate their advertising is to customers.“To succeed in the future that’s taking shape, companies must revisit every aspect of what they do and how they do it,” says Christopher Vollmer, Global Advisory Leader for Entertainment and Media, PwC US. “This means going ‘above and beyond’ in how they envision their business, generate revenues, create and organise their capabilities and build and retain trust.” Speed is vital, he continues. “For many companies, the models, assets, practices and capabilities that support their businesses today will simply not be enough in the future. Standing still is not an option.”