by Sam Davey, Leisure Development Partners (LDP)

Europe is one of the world’s most densely populated and economically developed regions. With almost 750 million residents and over 700 million international tourist arrivals, the continent has provided a solid foundation for the development of location-based entertainment.

This has fuelled the growth of theme parks, water parks, cultural venues, resort destinations, and indoor attractions over the past century.

This maturity is most evident in Western and Northern Europe. France, Germany, Belgium and the Netherlands collectively form one of the world’s most developed theme park markets. The UK and Scandinavia also boast strong markets. Across the region, per capita visit rates are among the highest globally.

Whilst these markets remain vibrant, opportunities for large-scale theme park development are increasingly rare. New investment tends to focus on small and mid-scale attractions, indoor experiences, and the enhancement of existing assets. However, the planned Universal theme park in the UK is a notable exception.

Attractions in Central & Eastern Europe

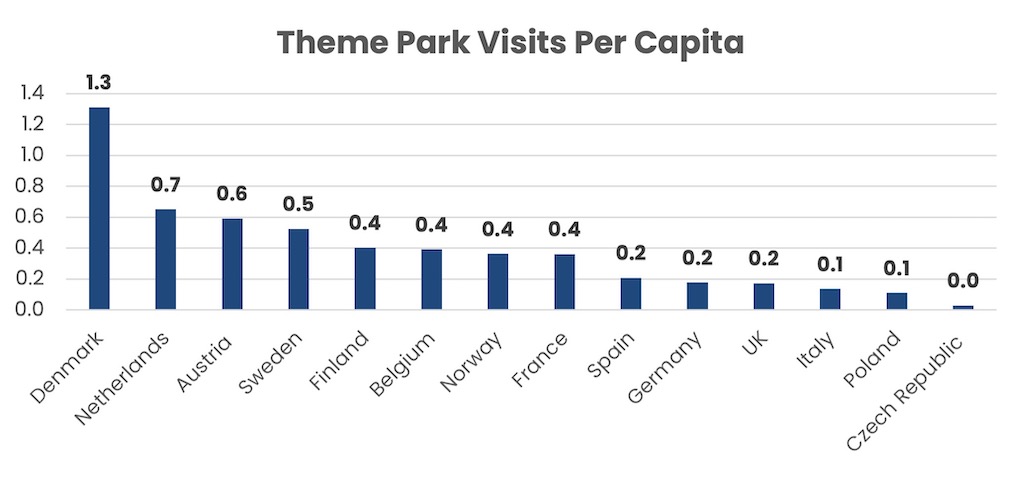

Looking eastward, the story is different. Lower population density and disposable incomes have resulted in a slower pace of development across Central and Eastern Europe. This is illustrated in the chart below, showing theme park visits per capita for a selection of European countries.

At the top of the chart, we mostly see Scandinavian and Western European countries. Meanwhile, only Poland and the Czech Republic make the list from Central Europe (though they still fall short of their Western and Northern counterparts).

Other countries, such as Romania and Hungary, have not made the list due to the lack of any major parks. While the metric focuses solely on theme parks, it serves as a useful proxy for the overall development of attractions of all scales across Europe.

Central Europe: a market on the rise

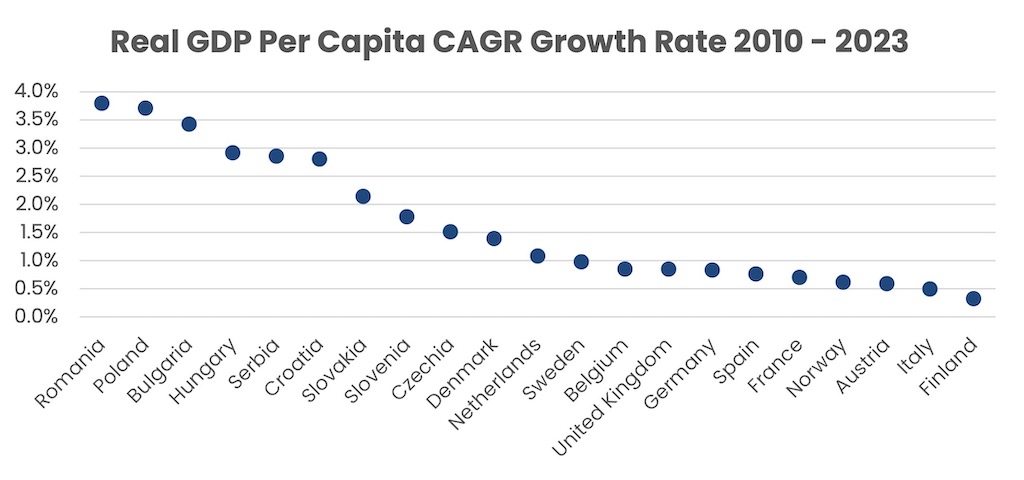

Central Europe represents one of the most promising growth areas for leisure and entertainment development. Economies across this region have posted strong GDP per capita growth and rising household incomes, outpacing larger Western economies over the past decade.

This is shown below, with Romania, Poland and Bulgaria exhibiting the strongest overall performance since 2010.

This economic growth is translating into increased discretionary spending, including on leisure and entertainment. As disposable incomes rise, households allocate a larger share of spending to recreational experiences. This fuels demand for attractions of all types.

At present, the region’s attractions industry still has significant room for growth. Large-scale theme parks are few, though there are successful examples, such as Poland’s Energylandia and several Majaland indoor parks. Indoor water parks and wellness facilities are highly popular, and most countries feature FECs, indoor play, and outdoor adventure parks.

Whilst the region is home to a plethora of world-class cultural experiences and historic sites, there is a noticeable lack of higher-quality commercial entertainment options and IP-driven attractions in many markets.

So, where are the opportunities?

Poland

Poland is the most advanced attractions market in the region. With strong GDP growth, a large population, and increasing tourist arrivals, the country continues to see investment in leisure and entertainment.

Parks like Energylandia have demonstrated that large-scale attractions can thrive here. Majaland has expanded with indoor and outdoor IP-based parks in Warsaw, Kownaty, and Gdańsk. Later this year, Hossoland, a major 400,000 sqm theme park, is set to open on Poland’s northern coastline.

Water parks are also very popular. This was underscored recently by a significant investment in the Suntago Water World complex, situated 45 minutes from Warsaw.

Despite this progress, a considerable portion of the population remains underserved. Opportunities persist in multiple markets across attractions of all scales and typologies.

At LDP, we have certainly seen strong interest in Poland, having worked on several assignments in recent years. Key markets include Warsaw, the capital and a major population and tourism hub, as well as Katowice, Łódź, Gdańsk, Kraków, and Wrocław, to name a few.

The Czech Republic

The Czech Republic also has a favourable outlook. With one of the highest GDP per capita in Central Europe, low unemployment, and a strong domestic tourism base (2.6 trips per person annually), the market offers potential for appropriately scaled attractions in key cities like Prague, Brno and Ostrava.

Majaland Prague, an IP-themed indoor park, opened in 2022. LDP has also worked on several other projects in Prague and elsewhere recently.

Whilst the country’s population of 10.8 million is modest by regional standards, several cities benefit from their proximity to neighbouring markets. Ostrava, for instance, is just a one-hour drive from Katowice, a considerable urban area in Poland. At the same time, cities to the west and north are well-positioned to attract cross-border visitors from Germany.

Romania

Romania is another market where LDP has been particularly active over the past ten years, with projects ranging from theme parks and water parks to smaller-scale commercial attractions across multiple cities.

While GDP per capita trails some neighbours across the region, the long-term growth has outpaced most, having risen by 3.8 percent per year since 2010. Most activity is concentrated in Bucharest, the country’s largest and most affluent market, and home to the highly successful Therme Bucharest spa, wellness, and water park.

However, we are also seeing growing interest in cities such as Cluj-Napoca, Constanța, and Brașov. As disposable incomes continue to rise among Romania’s 19 million residents, demand for leisure experiences is expected to increase, creating opportunities for a diverse range of attractions.

Hungary

Hungary has shown strong economic performance in recent years, despite particularly high inflation since 2021.

Both resident and tourist markets are concentrated in Budapest, where there is a healthy supply of attractions but perhaps a lack of high-quality indoor family entertainment. While Budapest offers clear opportunities, the markets outside of the capital are somewhat limited for major commercial developments.

Other smaller markets

Other small markets, such as Slovenia, Slovakia, and Croatia, also offer opportunities. Though their populations are smaller, they are also benefiting from rising incomes and limited existing competition. Opportunities exist for right-sized concepts such as family entertainment centres, adventure parks, or water parks.

Countries such as Bulgaria and Serbia, though progressing economically, still face some limitations in purchasing power, making the development of larger-scale, high CAPEX projects more challenging.

However, there are still opportunities in the right markets. Sunny Beach in Bulgaria, for instance, is a major tourist destination, featuring several water parks, an amusement park, and a variety of smaller tourist attractions.

Conclusion

Clearly, there are many opportunities across Central Europe for attraction development, from larger-scale water and theme parks, through to indoor commercial attractions. Rising disposable incomes, increasing international and domestic tourism, and relatively limited existing competition in many markets all point to strong growth potential across a range of attraction typologies.

This opportunity extends to both existing local operators looking to expand or diversify their offerings and to new entrants looking to establish a presence in new markets. For international brands and investors, partnering with experienced in-country partners can offer valuable local insight and help to navigate regulatory environments.

That said, these markets are not without their challenges. Price sensitivity remains a key consideration in many areas, particularly for larger, capital-intensive projects, and access to financing can pose a significant challenge. However, these risks can be mitigated with good planning and by completing a feasibility analysis early in the development process.

Ultimately, the key to success lies in tailoring each project to its market.

Ensuring the concept has a strong fit with local audiences, considering the level of local competition, scaling the project appropriately based on market demand, and aligning pricing with local purchasing power are all covered within feasibility and will ensure a robust business case.