In today’s fast-changing experiences industry, the landscape for tour, activity and attraction operators has shifted dramatically. A varied distribution strategy is now essential for survival and growth – not a nice-to-have.

For years, operators have worried that leaning into Online Travel Agencies (OTAs) will “cannibalise” their direct bookings.

It is an understandable fear, especially for businesses that invest heavily in their own websites and marketing, but the data increasingly shows this is an outdated assumption rather than a hard truth.

The cannibalisation myth, up close

From small local operators to headline attractions, many still assume OTA listings mainly steal customers who would have booked direct anyway. That belief has held many businesses back from digitising at scale and fully stepping into the modern experiences economy.

In reality, OTAs tend to bring in customers operators, including well-known attractions, who would not have reached on their own: people browsing in different languages, in new source markets, or in closed-audience channels, and crucially at the “inspiration” stage when they are still open to options.

In joint work with GetYourGuide, partners who joined the Bókun platform saw an average 36% increase in total revenue and a 31% increase in ticket sales in the 12 months after listing, combining both direct and OTA bookings.

Direct revenue rose by 14%, OTA revenue by 63%, with ticket sales up 18% via direct channels and 43% via OTAs. That's hardly the profile of a channel that simply replaces what you already have.

The billboard effect, finally proven for experiences

Hotels have talked about the “billboard effect” for years: appear on a major OTA and both indirect and direct bookings rise as travellers see you in more places and remember you when they are ready to buy.

Until recently, this was more analogy than proof for experiences, which is why the latest numbers from GetYourGuide’s Travel Experience Trend Tracker are so important.

What the findings really tell operators

The research is broad: 238 experience creators across eight categories, tracked over 24 months (12 before and 12 after joining GetYourGuide), supported by three independent research partners.

A few points stand out:

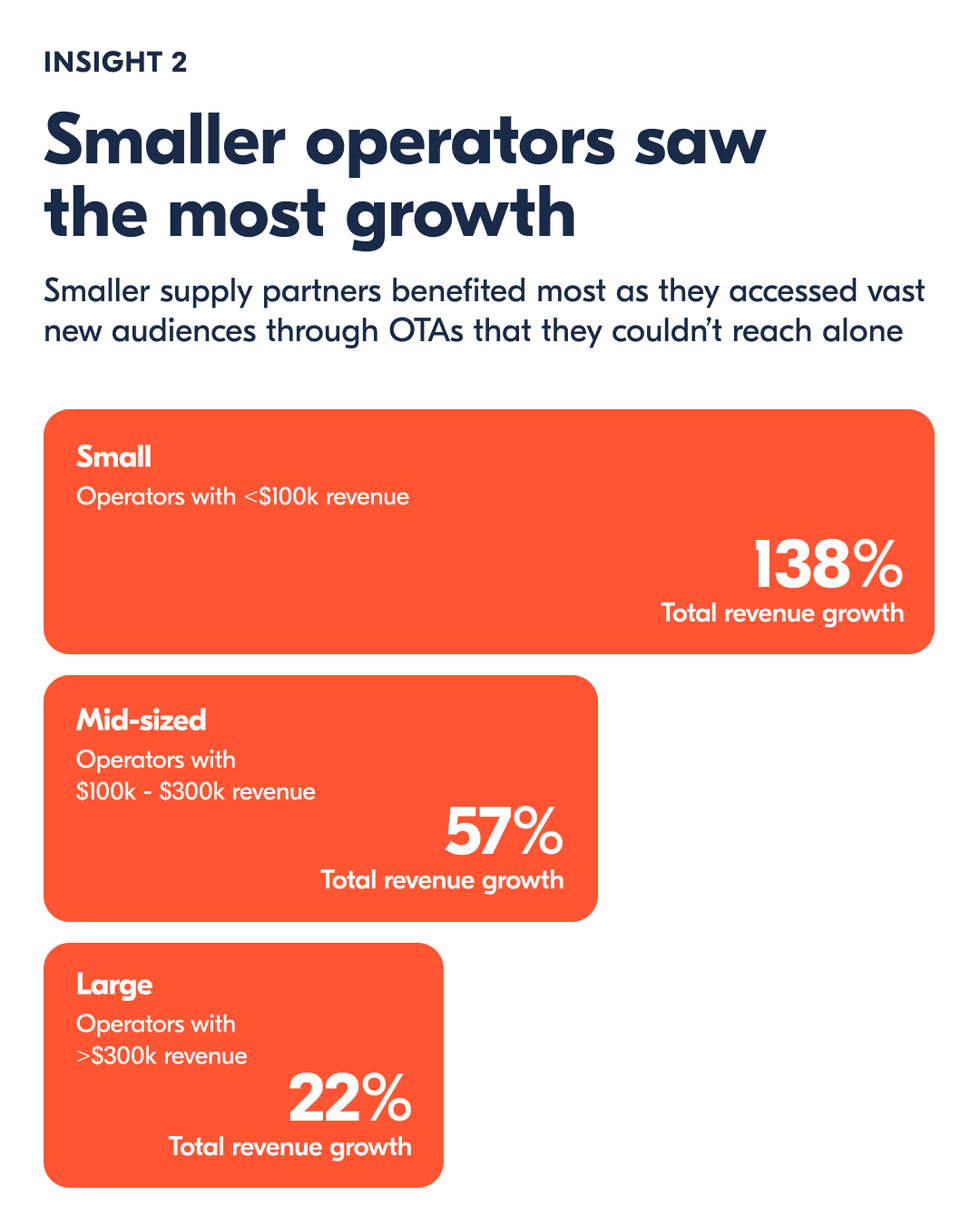

- Smaller operators gain the most headroom: those with annual revenue under $100k saw 59% total revenue growth and 47% ticket volume growth after joining.

- Larger, established suppliers still win: operators above $300k saw 33% revenue growth and 38% ticket growth, proving OTAs are a long-term lever, not just a lifeline.

- Even “multi‑OTA” suppliers benefit: operators already working with four OTAs still saw around 50% net revenue growth year‑on‑year after adding GetYourGuide, underlining that each OTA brings its own audience.

The conclusion is hard to avoid: the real risk today is not “doing too much with OTAs” but not doing enough, soon enough.

Why Bókun takes a strong view on distribution

Bókun has always treated distribution and connectivity as the backbone of a healthy experiences business. Global, regional and local markets are all fragmenting and growing; no single direct channel can keep up with where customers discover and book.

That is why so much emphasis is placed on plug‑and‑play connections to OTAs, the Bókun Marketplace, and tools like the booking agents area, giving operators broad reach without drowning them in admin.

As a Premium Connectivity Partner with GetYourGuide, recognised for technical quality and a very low error rate, Bókun sees daily how smooth integrations translate into more visibility, more partners and more revenue.

With average revenue uplifts of over a third after joining GetYourGuide, varied distribution is no longer optional. It is a competitive advantage.

See also: The digital imperative: why broad distribution is non-negotiable for attractions

As we look to the future

The conversation about OTAs needs to shift. Instead of asking, “Will they steal my bookings?”, more useful questions are:

- Which audiences am I missing by staying mostly direct?

- How can I use OTAs to test new products, markets or segments?

- What mix of channels gives me resilience if one source slows down?

Tours, activities and attractions all face the same reality: customers are planning across more channels, on more devices, with higher expectations than ever.

Operators that treat OTAs as amplifiers rather than threats, and build a diversified, data‑led distribution strategy, are already pulling away from the pack.

For attraction operators in particular, the risk is not “giving too much” to OTAs; it is quietly fading from view while others claim the digital high ground.

As a Tripadvisor company, Bókun helps operators manage bookings and sales channels in one place while connecting them to leading OTAs such as GetYourGuide and Viator.

The question is no longer whether diversified distribution is a good idea – it is how quickly you can build a strategy that lets OTAs grow your brand and booking numbers, and ensures your attraction is visible wherever future visitors are doing their research.